SERVICES

RETIREMENT & INVESTMENT PLANNING

Retirement & Investment Planning

We help you build a clear, confident path toward long-term financial security. Our role is to manage your investments in a tax-efficient and low-cost way, so you always know your money is working hard for your future.

CLARITY BETWEEN TODAY AND TOMORROW

We separate your near-term needs from long-term goals like retirement, so you always know what is protected for today and what is growing for the future.

WHAT THIS MEANS FOR YOU

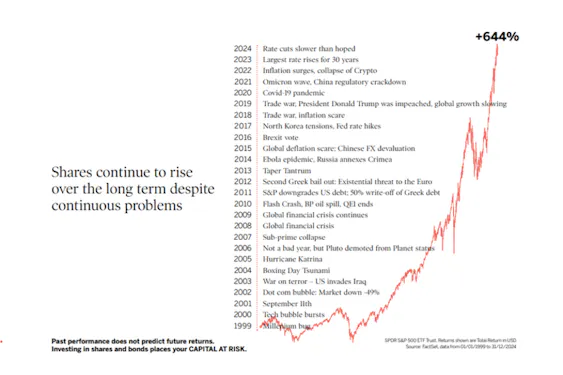

STRONGER LONG-TERM GROWTH POTENTIAL

Any surplus earmarked for the future is invested in low-cost, globally diversified equity portfolios. This gives you a much better chance of achieving real, inflation-beating returns over time.

WHOLE-OF-MARKET INVESTMENT ACCESS

Being fully independent means we select the most suitable fund managers, geographies and asset classes across the entire market, not just a restricted panel.

TAX-EFFICIENT STRUCTURING

We make full use of the right tax allowances and wrappers so more of your money stays invested and working for you.

THE IMPACT

Everything in your financial life narrows down to one question.

"Do I have enough to live the life I want?"

Our planning helps you feel confident that the answer can be yes, not by guessing, but through clear modelling, disciplined investing and ongoing guidance.

FREQUENTLY ASKED QUESTIONS

Your questions, answered.

Will I lose my pension if the stock market crashes?

In most cases, no. A stock market crash does not mean you lose your pension. Pensions are long term investments, often spread over hundreds of companies across the world. While markets do fall, that volatility is a normal part of investing.

It is important to understand that market crashes are temporary and investments into one's pensions are for longer periods, in most cases for decades. Historically, markets have always recovered given enough time. If you have 10 years or more until retirement, the historical data shows that the chances of permanently losing money in a well-diversified pension are very low.

You only actually lock in a loss if you sell your investments after a crash. If you stay invested and allow time for recovery, markets have historically bounced back.

What is a good monthly retirement income in the UK?

A good monthly retirement income in the UK is one that allows you to maintain a comfortable lifestyle without worrying about day-to-day expenses. For most people, this means having an income similar to what they spend now, but often slightly less, as some costs reduce in retirement.

As a broad guide:

• Minimum lifestyle: around £1,300–£1,500 per month (after tax)

• Moderate lifestyle: around £1,800–£2,200 per month

• Comfortable lifestyle: £2,500+ per month

These figures are per person, not per household.

The amount you need depends on:

• Whether your home is mortgage-free

• Your desired lifestyle (travel, hobbies, eating out, etc.)

• Health and care costs

• Whether you retire single or as a couple

According to the Office for National Statistics, average UK household spending is around £620 per week, but retirees typically spend less than working households, as costs like commuting and saving for retirement usually stop.

Also, the full UK State Pension currently provides a base income, but on its own, it usually covers only basic living costs. Most people need private pensions or other savings on top to achieve a comfortable retirement.

What is the 4% rule in retirement in the UK?

The 4% rule is a simple guideline used to estimate how much you can withdraw from your retirement savings each year without running out of money too soon.

In basic terms, it suggests that you can withdraw 4% of your pension and investment pot in the first year of retirement, then increase that amount each year in line with inflation.

An Example of how the 4% rule would work:

Many couples retiring in their 60s will plan for a retirement for another 30 years. If they have a combined pension and Investment pot worth £500,000 and they start withdrawing 4% from year 1, then:

• In year 1, they withdraw £20,000;

• From year 2 onwards, they adjust this amount in line with inflation;

• The aim is for the money to last for the next 30 years

The rule was made using historical data of the US market and assumes a long-term balanced investment portfolio. However, it may not hold true for UK markets.

The limitation of the 4% rule is that it could be ineffective due to factors such as:

• Tax on pension withdrawals

• Inflation

• Investment returns

• Market crashes in early retirement

Hence, the 4% rule is a useful thumb rule, but it is not a one-size-fits-all solution. In the UK, a flexible, personalised retirement income plan is usually more reliable than relying on a single percentage rate of withdrawal.

It is also possible that 4% of your portfolio will not be enough to fund your lifestyle for a year – even when combined with the state pension.

What are the three most common pitfalls in retirement planning?

The three most common mistakes people make when planning for retirement are starting too late, investing poorly, and underestimating how long retirement may last.

Starting retirement planning too late

One of the biggest retirement planning mistakes is not starting early enough. The earlier you begin saving, the more time your money has to grow through compounding. Delaying contributions even by a few years can significantly reduce the size of your retirement pot.

UK pensions are particularly effective because they offer:

• Income tax relief on contributions

• Tax-free growth while invested

Starting early often requires smaller monthly contributions to achieve the same retirement outcome.

Poor investment choices or inappropriate asset allocation

Another common pitfall is investing unwisely, either by being too cautious or taking the wrong level of risk.

For long-term goals like retirement, holding too much in cash can mean your money fails to keep up with inflation. A well-diversified, equity-oriented portfolio can provide long-term growth and help preserve purchasing power.

Using appropriate vehicles such as pensions and ISAs, combined with a suitable asset allocation, is crucial for long-term success.

Underestimating retirement length and future expenses

Many people underestimate how long retirement may last and how much they will spend. With improvements in healthcare and living standards, it’s increasingly common for people to spend 25–30 years or more in retirement. Retiring in your early 60s could mean your savings need to last well into your late 80s or beyond.

Failing to plan for longer life expectancy, inflation, and rising healthcare & lifestyle costs can increase the risk of running out of money later in life.

What is the hardest thing about retirement?

For many people, the hardest part of retirement is not financial. It is the loss of meaning, purpose, and routine. After spending decades working, raising a family, and following a structured daily schedule, retirement can feel like a sudden change in identity.

Many retirees struggle with:

- Loss of routine – no fixed schedule or reason to structure the day

- Loss of social interaction – fewer daily conversations with colleagues

- Loneliness – children moving out, reduced social circles

- Loss of purpose – work often provides a sense of achievement and identity

- Life changes – such as divorce, illness, or the loss of a partner

These changes can come as a surprise, even to people who were excited about retiring.

Why does this happen?

One reason is that many people spend years focusing on work and financial goals, while postponing personal interests, hobbies, and passions until “after retirement”.

When retirement finally arrives, the structure disappears — but the new purpose hasn’t yet been built.

How to make retirement more fulfilling

A smoother transition into retirement often involves planning beyond money, such as:

- Developing hobbies or interests before retiring

- Maintaining social connections and routines

- Creating a sense of purpose through volunteering, part-time work, or mentoring

- Gradually transitioning into retirement rather than stopping abruptly

Financial security supports retirement, but fulfilment comes from how you spend your time.

How much does the average person have in savings when they retire in the UK?

Source: Pension wealth: wealth in Great Britain, 2020-2022, ONS, published January 2025. This only includes people with pension wealth; those that have zero pension savings are excluded in the figures.

Meanwhile, PensionBee gave the following figures to MoneyWeek in January 2026 showing the average pension of its customers:

• Aged under 30: £3,745

• Aged 30-39: £10,660

• Aged 40-49: £23,311

• Aged 50 and over: £42,578

THE GAP BETWEEN REALITY AND WHAT IS NEEDED

The PLSA's Retirement Living Standards (2025) set out three tiers of retirement lifestyle. For a one-person household: a minimum standard covering basic needs with little left over costs £13,400 per year. A moderate standard, which includes a small car and a two-week European holiday, costs £31,300. A comfortable standard, with longer holidays, more flexibility and regular leisure spending, costs £43,900. All figures are after tax and assume no mortgage or rent costs.

To achieve even a moderate lifestyle, a single person would need a pension pot of roughly £330,000 to £490,000, yet the average pension wealth for any age group, including those already approaching retirement, falls well short of this figure.

What are the biggest expenses in retirement?

Most people expect their costs to fall when they stop working. In practice, the picture is more complicated.

1. Housing and household bills

For homeowners who have paid off their mortgage, housing costs reduce but do not disappear. Council tax, utility bills, maintenance, and home improvements continue and typically rise with age.

2. Food and everyday living

The ONS Living Costs and Food Survey confirms food as one of the largest weekly expense categories for retired households, and this figure does not fall significantly just because someone stops commuting.

3. Health and long-term care

This is the expense most people underestimate most severely and the one with the greatest potential to derail a retirement plan entirely. While NHS treatment remains free at the point of use, social care is not. It is means-tested, and the thresholds are low. Anyone with assets above £23,250 in England is expected to fund the full cost of their own care.

4. Tax

Retirement income is not tax-free. The State Pension, pension drawdown, and annuity income all count as taxable income. Only the first 25% of a pension pot can be taken tax-free. Poorly structured withdrawals can push retirees into higher tax bands, reducing net income significantly. HMRC has specific rules governing how pension income is taxed, and taking professional advice before accessing a pension is one of the highest-value things a person can do.

5. Other discretionary spends

5.a Travel and leisure and

5.b Supporting family

What is the golden rule of retirement planning?

There is no single rule written in law or handed down by a regulator. But across financial planning, there is a clear and consistent answer that emerges from decades of research and practice:

1. Start Early

The reason is compound growth. Money invested today does not just grow, it grows on its growth. Each year of delay does not simply subtract one year of saving; it removes one of the most valuable years your money could have been working for you. Saving just £100 a month from age 25 can grow to over £150,000 by age 65 at a 6% annual return. Wait until age 40 to start, and the same monthly contribution produces only around £50,000, roughly a third of the outcome.

2. Don't just save…Invest instead

Money left in cash loses value in real terms over time. Inflation, even at modest levels, erodes purchasing power year on year. A pension or ISA invested in a diversified, appropriately structured portfolio has historically produced returns that outpace inflation over the long term. Cash would not and frankly, cannot.

3. Keep reviewing

Life changes, and so does tax rules.

Start sooner and save more than feels comfortable. Everything else in retirement planning, like investment choice, tax efficiency, drawdown strategy, etc., builds on that foundation.

Future Value = Present Value X (1 + rate or return) ^ number of years of investment

In the above equation, you can control your input and the number of years you can give to your investments. You cannot control the rate of return, nor the outcome.

Is paying 1% to a financial advisor worth it?

What the research says….

Multiple independent studies have attempted to quantify what a good financial adviser actually adds in measurable terms. Vanguard's research estimates that advisers can add over 3% per annum in net returns for their clients through behavioural coaching, spending strategy, and portfolio rebalancing, none of which has anything to do with fund picking.

Russell Investments puts the figure higher, at 4.4% per annum, through a combination of preventing behavioural mistakes, financial planning, and tax-smart advice.

The International Longevity Centre, which has been tracking this over multiple years in the UK, concluded that those who take ongoing financial advice end up with pension wealth 50% greater than those who take only one-off advice.

A University of Montreal study found that the savings of an advised client are 2.73 times larger over a 15-year period compared to a non-advised client.

If an adviser is adding 3 to 4% per annum in identifiable value, a 1% fee is not a cost. It is one of the better investments you can make.

But….

What the percentage figures cannot capture is arguably the more important part of what a good adviser actually does.

There is real value in having someone in your corner who understands your full financial picture, how your investments interact with your tax position, your family circumstances, your business interests, and your longer-term goals and aspirations. Most people do not lack information about money. What they lack is someone to help them apply that information to their own situation clearly and calmly.

There is also the behavioural dimension. Markets & tax-related changes, life events happening. At each of those moments, the instinct is often to do something, like to react, to move money or to make a change. A good adviser's most consistent job is to act as a steady hand that helps you hold the course when the headlines are making too much noise and making sure that decisions get made deliberately rather than emotionally. The research consistently shows that the most expensive mistakes investors make are behavioural, not technical.

And there is the simple comfort of knowing that someone competent is keeping watch. Not in a passive, annual-review sense, but as a genuine point of contact when questions arise. Questions around pension access, an inheritance, a job change, a business exit, or simply the uncertainty that comes with getting older. For many people, the value of having a trusted person to call is not something they can put a price on, but they would not want to be without it.

The question worth asking

The better question is perhaps not "is 1% worth it?" but "what am I actually getting for it?" A good adviser should be able to answer that clearly in terms of the plan they have built, the tax they have helped you save, the mistakes they have helped you avoid, and the ongoing relationship they provide.

If the answer is just a managed portfolio and an annual letter, that may not justify the fee. If the answer is a financial plan built around your life, proactive tax structuring, someone who knows your situation, and a trusted point of contact for the years ahead, then that is a different proposition entirely.

What does it mean to be tax efficient?

Being tax efficient means making deliberate use of every legitimate allowance, relief, and structure that HMRC makes available so that more of your money builds toward retirement, and less is lost to tax along the way. The opportunities available to you depend significantly on how you earn.

For employees with modest to middle incomes

The most impactful starting point is your workplace pension. Under salary sacrifice, your contribution is treated as being made by your employer, which means you pay less income tax and National Insurance on a lower salary, and your employer typically pays less National Insurance too. This makes salary sacrifice one of the most efficient ways to build a pension for employees at any income level.

Note: from April 2029, salary sacrifice pension contributions above £2,000 per year will attract employee and employer National Insurance contributions on the excess. This change was announced in the 2025 Budget, which is worth being aware of now.

If your employer does not offer salary sacrifice, contributing to a personal pension via relief at source still earns basic rate tax relief of 20%, added automatically by HMRC to every contribution. Your employer contributions on top of your own are genuinely free money and not using them in full is one of the most common financial mistakes in the UK.

Beyond pensions, the Stocks and Shares ISA allowance of £20,000 per tax year provides a tax-free environment for investment growth and withdrawals with no capital gains tax or income tax on returns. For parents, a Junior ISA adds a further £9,000 per child per year in the same tax-free wrapper.

Sources: HMRC Tax on savings and investments; GOV.UK — ISA allowances

For higher earners (income above £50,270 and particularly £100,000 & above)

Higher and additional rate taxpayers receive 40% or 45% pension tax relief, respectively, but this does not happen automatically. If you are a higher-rate taxpayer, there is a good chance you are not claiming all the tax relief you are entitled to. Higher earners in the UK miss out on hundreds of millions of pounds in unclaimed pension tax relief every year simply because it is not added automatically. The extra relief above the basic rate must be claimed via self-assessment.

For those with income between £100,000 and £125,140, the position is particularly powerful. Within this income band, the personal allowance of £12,570 is reduced by £1 for every £2 earned over £100,000. A pension contribution in this range effectively reclaims some or all of the personal allowance, producing an effective tax relief rate of 60% on those contributions. This is one of the most valuable and underused reliefs in the UK tax system.

The ISA and JISA allowances remain fully available and valuable at this income level. For those who have maximised pension contributions or face the tapered annual allowance (which reduces the £60,000 annual pension allowance for those with adjusted income above £260,000), VCTs and EIS can provide a parallel investment route with meaningful tax incentives.

EIS investments provide 30% income tax relief, the ability to defer capital gains tax, and may also qualify for Business Relief for inheritance tax purposes after a two-year holding period. VCTs provide income tax-free dividends and capital gains exemptions on exit, with income tax relief currently at 20%. Both carry significant investment risk and are unsuitable for everyone; they are tools for those who have already maximised conventional routes and have the capacity to accept illiquidity and potential capital loss.

Sources: GOV.UK Tax relief for investors using venture capital schemes; HMRC EIS and VCT changes from April 2026;

For business owners and company directors

The most structurally efficient approach for a director is to make pension contributions through the company rather than personally. Employer pension contributions are not subject to National Insurance and can generally be deducted as a business expense to reduce the amount of corporation tax payable, provided they are wholly and exclusively for business purposes. This means a £10,000 director pension contribution made by the company saves corporation tax at 25% and avoids National Insurance entirely, making it considerably more efficient than paying the equivalent as salary or dividend and contributing personally.

Relevant Life Cover is another structure worth knowing. A policy taken out and paid for by the company provides life assurance for the director, with premiums typically treated as a deductible business expense, saving corporation tax and national insurance on the premium amount. It sits outside the director's estate for inheritance tax purposes, adding a further layer of planning value.

Beyond that, the same ISA, JISA, and, where appropriate, VCT and EIS routes available to high earners apply equally to business owners, particularly those who take a combination of salary and dividends and need to build wealth in a tax-efficient structure outside the business.

Sources: HMRC Business Income Manual BIM46000 (employer pension contributions); GOV.UK Relevant Life Policies

The principle across all three

Tax efficiency in retirement planning is not about finding loopholes but about using the structures that HMRC has designed precisely for this purpose. The goal is to ensure that every pound you save toward retirement is working at its full pre-tax value, growing in a tax-advantaged environment, and drawn down in a way that minimises the tax you pay in retirement itself.

Getting this right, particularly the interaction between pension contributions, the personal allowance, salary sacrifice, and ISAs, is where independent financial advice adds the most measurable value.

Can I retire at 60 with 500K in the UK?

Maybe..maybe not, but whether £500,000 is enough depends entirely on the life you are planning to fund and for how long. Retiring at 60 means you cannot access the State Pension until 67. That gap has to be bridged from your own savings. At 60, you could reasonably be planning for a 30-year retirement.

The three scenarios

The PLSA's (Pensions and Lifetime Savings Association) 2025 Retirement Living Standards set out three tiers of annual spending after tax, assuming no mortgage or rent costs.

Modest lifestyle requiring £13,400 per year (one person) covers the basics like household bills, food, a week's UK holiday, and no car. At this level, £500,000 invested and drawn down at a 4% withdrawal rate generates £20,000 per year, which is comfortably above the minimum threshold and sustainable over 30 years if the portfolio continues to grow. Once the State Pension kicks in at 67, the pressure on the pot reduces significantly. At this lifestyle level, £500,000 is likely sufficient for a single person.

Moderate lifestyle requiring approximately £31,700 per year (one person) includes a small car, a two-week European holiday, and more flexibility on food and clothing. Standard Life estimates that a single person needs around £439,000 in savings to fund a moderate retirement, but that assumes retirement at State Pension age, not at 60. Retiring seven years earlier means drawing down with no State Pension income for that period, which substantially accelerates depletion. At this spending level, £500,000 is tight for a single person and insufficient for a couple without additional income sources.

Comfortable lifestyle requires about £43,900 per year (one person), including long holidays, regular home improvements, eating out regularly, and a generous clothing budget. A single person needs a pension pot of between £540,000 and £800,000 to fund a comfortable retirement starting at State Pension age. Starting at 60 with no State Pension for seven years, £500,000 falls short at this spending level for most people.

What else affects the answer

Beyond lifestyle spending, several factors can materially change how long £500,000 lasts.

Health and life expectancy matter more than most people acknowledge. Retiring at 60 in good health with longevity in your family means planning for 35 years or more. Conversely, if health is already a concern, a shorter horizon changes the calculation entirely and may also mean higher medical or care costs in later years.

Family responsibilities are often the biggest wildcard. University costs for children typically range from £9,000 to 12,000 per year in tuition alone, plus maintenance can easily run to £40,000 to £50,000 per child if funded by a parent. Elderly parents requiring care or financial support can add further unplanned drain. Neither of these features is in the PLSA's standard figures.

How the money is invested is equally important. £500,000 sitting in cash will lose real value every year to inflation. Invested in a diversified portfolio targeting 5–6% annual growth, with a disciplined withdrawal strategy, the pot behaves very differently. The sequencing of withdrawals and which pot to draw from first, how to use ISAs and pension income together to minimise tax, can extend a retirement fund meaningfully.

For a single person with a modest to moderate lifestyle, no major outstanding family financial commitments, a mortgage-free home and a sensibly invested portfolio, £500,000 at 60 is workable. For a couple, someone with a comfortable lifestyle in mind or anyone with significant family financial responsibilities still ahead, it is likely to fall short or require careful structuring to make it last.

The only way to know for certain is to model it properly against your specific circumstances.

What is investment planning?

Investment planning is the process of deciding how to put your money to work in a way that is aligned with your goals, your timeframe, and the level of risk you are comfortable with.

It’s about Goals

Before any investment decision is made, the first question is always, what is this money for?

The answer shapes everything else.

Money set aside to buy a property in three years needs to be managed very differently from money being built up for retirement in twenty-five years.

Short-term goals generally require lower-risk, more liquid assets such as cash and bonds.

Long-term goals can justify a higher allocation to equities, which carry more short-term volatility but historically deliver stronger growth over time.

It’s about understanding the risks.

Risk in investment planning has two dimensions that are often confused.

The first is your attitude to risk. How much volatility are you psychologically comfortable seeing in your portfolio?

The second is your capacity for risk. How much loss could you actually absorb without derailing your financial plans?

Both matter, and a good investment plan addresses both honestly.

A sound investment strategy starts with an asset allocation built on reasonable expectations for risk and returns, using diversified investments to avoid exposure to unnecessary risks.

Asset allocation and diversification

Once goals and risk are established, the next step is deciding how to spread money across different asset classes, viz., equities, bonds, property, cash, and alternatives.

This spread of assets and the proportions held in each is called asset allocation.

Choosing the right wrappers

In the UK, where you hold your investments is almost as important as what you hold.

Using tax wrappers such as ISAs and pensions is one of the most effective tools available.

They protect investment growth and returns from income tax and capital gains tax and allow rebalancing without triggering tax charges.

Rebalancing and ongoing review

Investment planning is not a one-off event.

Life changes, tax rules change, and financial goals evolve.

A plan built at 40 may need significant adjustment at 55.

Regular reviews tied to real life rather than just to market performance are what keep a plan working.

The Office for National Statistics (ONS) has data on how much the average pension pot is worth for seven age groups.

Age group

16-24

25-34

35-44

45-54

55-64

65-74

75+

Average pension wealth

£5,500

£18,800

£39,500

£80,000

£137,800

£145,900

£59,700